May 30, 2024

Credit Managers' Index rebounds in May

Annacaroline Caruso, CICP, editorial associate

NACM’s Credit Managers’ Index (CMI) improved 2.6 points to 54.4 in May, regaining ground from last month.

Why it matters: The CMI has showed no clear trend of improvement or decline in the last two years since the world emerged from the pandemic, but business outlook remains pessimistic.

What NACM’s Economist says: “The CMI oscillates between being on the precipice of recession to solidly in expansion,” said NACM Economist Amy Crews Cutts, Ph.D., CBE.

- “A little deeper look, and the survey respondents indicate sales are continuously improving and there is no indication that recession risk is even present,” Cutts added.

- Yes, but: “The number of accounts placed for collection has consistently been reported as rising for about a quarter of respondents each month for the past 24 months, indicating a lot of weakness in business trade.”

The index of favorable factors gained 3.4 points to 61.1.

- Three of the four factors improved while one remained the same.

- Sales improved 9.5 points year-over-year.

The index for unfavorable factors improved by 2.0 points to 49.9, marking its second month in contraction territory where it has been for 10 of the past 12 months.

- Dollar amount beyond terms recovered from the steep drop in April, marking a 7.2-point improvement back into the expansion zone with a value of 51.0.

- Accounts placed for collection is at 44.9 this month, marking its 24th month in contraction territory.

What CMI respondents are saying:

- “Customers are looking for longer credit periods across the globe. Voice traffic is reducing.”

- “The number of slower pay-when-paid contractual payments continues to be on the rise.”

- “We have some divisions that continue to show downward trends and a few others that performed better than last month. There seems to be no rhyme or reason to the ups and downs.”

- “New customer activity is picking up prior to this time last year. We are increasing capacity at our plants; however, we remain below budget.”

- “High interest rates are killing small and medium businesses, and this makes the life of anyone in Credit & Collections or Finance that much harder.”

- “We have started our busy season. Several customers caught up on their past due accounts.”

Sign up to receive monthly CMI survey participation alerts. For a complete breakdown of manufacturing and service sector data and graphics, view the May 2024 report. CMI archives also may be viewed on NACM’s website.

Outsourcing: Fact or fiction

Kendall Payton, editorial associate

Outsourcing is a common business practice among companies that use external providers to complete business processes and tasks. Outsourcing became a recognized business strategy in the 1990s as companies shifted the responsibility of some in-house processes to outside firms. Some companies use a shared services model, staffed by their employees, where like business functions are consolidated into a single unit that operates as its own entity to deliver services to the entire organization.

Why it matters: Oftentimes, a company will outsource to cut labor costs, manage risk or to take advantage of global supply chains and specialized production capabilities. Outsourcing is also used by companies that want to focus on the core aspects of the business, leaving the less critical operations to outside organizations.

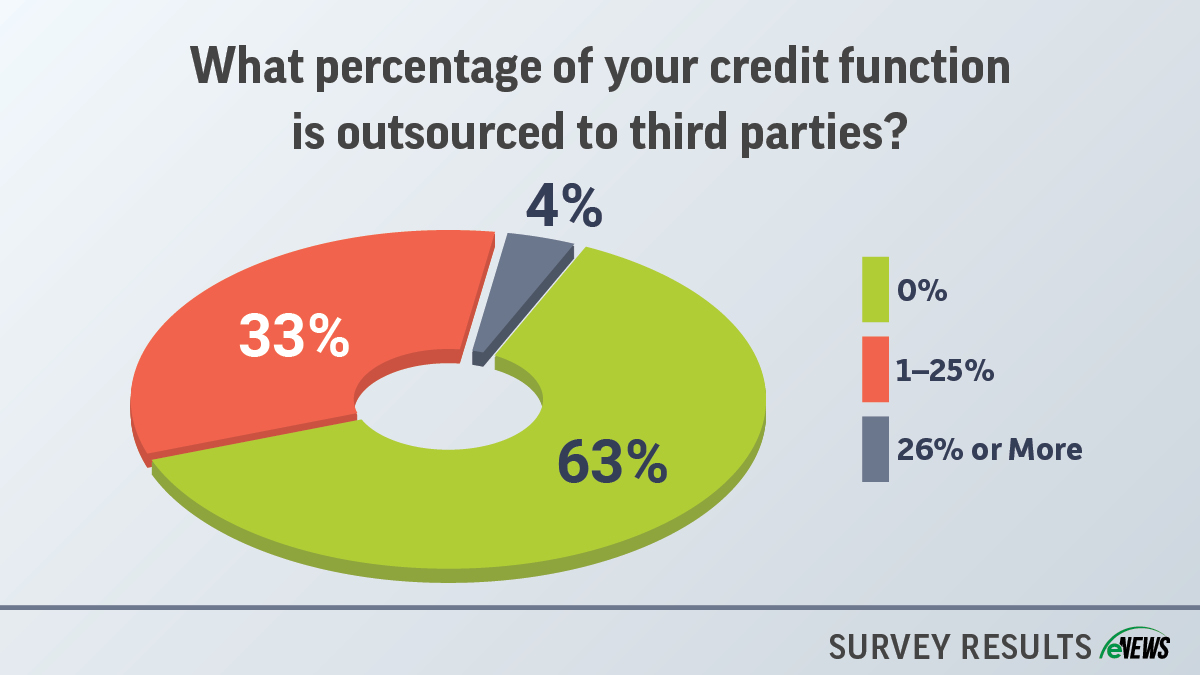

By the numbers: A recent eNews poll revealed that 33% of credit departments outsource between 1%-25% of the credit function.

Some companies will outsource their entire credit department while others may only outsource specific functions. While outsourcing tends to get a bad reputation because of the potential downsides, there are a few common fears that can be debunked.

Myth #1: “The company will find cheaper labor offshore. There goes my job!”

Debunked: Not necessarily. In most cases, outsourcing your role can be a motivator to enhance or add onto your skills and reevaluate your value in the company. Many supporters of outsourcing believe it can provide an incentive for businesses to pour resources into the areas in which their employees are most effective. Outsourcing also helps maintain free-market economies globally. It is all about perspective. Outsourcing can also create the opportunity to build a partnership with the third-party team—making them an extension of yours.

As a credit professional who is currently implementing RPAs or robotic process automation in his department to help with automation, Christopher Finley, CICP, global credit manager at Club Car LLC (Troutman, NC), said he is outsourcing some team functionality to India.

“I have two bots that are now running, and to me that’s a form of outsourcing because one bot took an eight-hour day of work and consolidated it into a 20-minute review process for my team,” Finley said. “Because of its success, we are now trying to implement it elsewhere within the business, and I am fighting the groupthink fear of the potential for bots to eliminate positions within the organization. We need our team’s providing more hands-on service to our customers—and if those types of repetitive tasks can be simplified, we enable the team to focus on more value-added tasks for the business.”

Myth #2: “It’s so much cheaper to outsource.”

Debunked: Though many companies turn to outsourcing as a way to cut costs, there is even more cost involved in replacing an employee. It takes time, money and investment into onboarding and training a whole new team on the ins and outs of each customer. Outsourcing can also be more expensive in terms of:

- Task complexity

- Location of the outsourcing entity

- Company internal costs

- Communication issues due to cultural mismatches

“Most companies will turn to outsourcing tasks such as collections or tasks that are considered the easy stuff,” said Charles Edwards, Jr., CCE, vice president of credit operations at SRS Distribution Inc., (McKinney, TX). “For example, calling customers with a smaller balance and small amounts of past dues are easier than facing the bigger customers where you want to retain the relationship. I think most of the larger companies are starting to outsource parts of their credit collections functions, accounts payable and accounts receivable.”

Myth #3: “Outsourcing is 100% safe to implement.”

Debunked: Turning to a third party does not do away with liability. In the event of any compliance issues or exposed risk, your company is still at fault if the third party gets into legal trouble. But not only does the risk exist in legal bounds, it can also impact the ability to collect. For example, if you give your entire collections function to the outsourced party, their responsibility and primary purpose is going to be to collect the dollars—not necessarily to retain the customer. If you have a longstanding relationship with a certain customer and they suddenly have a downturn in their sales, the third party will not pick up on those small yet notable differences.

“If the only objective is to collect those dollars, an outsource might not be as easy or as friendly to that customer as they could be to try and maintain that relationship,” said Edwards. “If the collections function was in-house, you know you would make arrangements such as a payment plan or use some other process to try and maintain that customer somehow.”

The bottom line: Outsourcing is a widely used business strategy, with benefits such as cost reduction and risk management, however, its effectiveness largely depends on the specific needs of the company.

How credit holds impact a customer relationship

Jamilex Gotay, editorial associate

Credit holds temporarily suspend or reduce credit limits for customers who miss payments or exceed their credit limit.

Why it matters: Although often used as a last resort, implementing credit holds is necessary as it aids in mitigating risk, ensuring financial stability and maintaining positive customer relationships.

Credit hold criteria and management vary by industry and company. For instance, Chelsea Hirn, director of credit operations at KGP Companies (Faribault, MN), has an internal automated system that places accounts on hold if customers exceed their credit limit or are past due, without direct notification to the customer.

“We're able to look at each account, being mindful of any deadlines or anything that might affect the customer,” Hirn said. “But we also reanalyze and assess risk and then release them as warranted. For each of the accounts that go on hold, there is a sales rep to review it.”

Because of her automated system, Hirn can inform the customer before they have to place the account on hold. “If they can’t get their account current in this specific period of time, we would either grant a higher credit limit or get certain assurances or get a payment in advance to decrease the credit or prepaid on that particular order.”

Jon Hanson, CCE, CCRA, VP, director of corporate credit at OVOL USA (Carrollton, TX), uses a trigger point system that may cause customers to go on credit hold such as:

- The order exceeds the credit line.

- The customer is past due.

- The customer is inactive.

The customer service team then tells the credit team which accounts need to be put on hold. But before any action is taken, the credit department carefully reviews the accounts and talks to the sales team in case they have more information.

“If a customer hasn't bought from us in over six months, even though the order may be under the credit line, it's going to make us look at it,” Hanson said. “We may conduct a background check, update the file or reach out to NACM for trade credit reports. But quite frankly, we see credit holds as an opportunity to communicate and get to know our customer.”

Some credit professionals use an exception-based credit order review system. Here’s an example of parameters for exception-based holds:

- Credit limit: If an order causes a customer to exceed their credit limit, the order will be placed on hold until a credit manager can review and release it. The credit manager will either make an exception (project-related, temporary circumstances, dispute or claim) or increase the customer’s limit after a review.

- Past-due balance: A balance that was over 30 days past due would go to the credit manager for review. The credit manager would release the order based on account status and communication with the customer.

These parameters can be changed by the credit manager at any time if within their delegation of authority. Some credit managers have key customers exempt from any order restrictions.

Yes, but: If not properly managed, credit holds can strain or even jeopardize customer relationships, which is why it is vital that credit professionals navigate credit holds with caution.

“It’s all about managing risk and maintaining the balance between meeting sales targets and promoting a clean A/R,” said Asha Weekes, ICCE, senior manager, credit at Gildan (Christ Church, Barbados). “Having good internal and external relations will facilitate this. It involves the customer, sales, customer service and the credit/AR collections teams.”

Weekes’ enterprise resource planning (ERP) system automatically places orders on hold when the customer is over their credit limit. It sends a message to the customer service team, who in turn reach out to the credit team to review and advise.

This hold, however, is not communicated to the customer unless it is required. “It may be a case of funds being received but not yet booked to their account,” Weekes said. “However, should we need to reach out, it would be a friendly reminder from the credit team that they have extended their limit, and an order is pending. Afterwards, we discuss the next steps. But it’s important to note that we also have a few low-risk customers exempt from the automatic hold.”

Tips for better customer relations:

- Make sure credit limits are up-to-date and realistic.

- Ensure your customer service team or online ordering system uses clear language. An order review differs from a credit hold, and your ERP should reflect this.

- Make sure that any disputed past-due A/R is coded so that it does not cause any credit holds due to the automated exception.

- Make sure that the customer is notified promptly if their account is on hold. Holding customer orders to get their attention without any prior notice is not good practice.

- Notify sales immediately if a customer is placed on hold. It is important to ensure they are informed and not caught off guard.

- Don't discuss credit issues with buyers or order placers if you're in customer service.

The bottom line: Implementing credit holds is important for mitigating risk and maintaining financial stability, but it requires careful management.

Top factors driving job satisfaction in credit management

🎙️ On the latest episode of NACM's Extra Credit podcast ... Job satisfaction is the key driver of positive results.

Read more...

Emerging Leader Award 1

"I hope this recognition inspires others to pursue their leadership potential as I feel everybody has greatness in them and we all have something great that we can achieve," said Brian Wallace, director of corporate credit at N.B. Handy Company (Lynchburg, VA).

Read more...

Emerging Leader Award 2

"In my credit manager role, I have learned that my resilience, my strength and my determination are my strongest assets in my career growth," said Brittany Yvon, CBA, CICP, credit manager at OMG, Inc. (Agawam, MA).

Read more...

Tips for hiring new credit managers

Kendall Payton, editorial associate

Credit professionals in the B2B industry have a wide range of responsibilities in their role. Whether you are a credit analyst, credit manager, risk analyst or any synonymous title to those listed—there are a few aspects that all professionals in credit have in common: assessing creditworthiness, mitigating risk and optimizing company sales.

Why it matters: Finding the right job is important for both the jobseeker and employer. Typically, job seekers want to join a company that will use their skills to the fullest while also being able to receive benefits (such as PTO, insurance and more). But what are some of the key qualities credit managers look for when hiring a potential candidate?

By the numbers: According to a recent eNews poll, 45% of credit professionals look for a candidate’s willingness to learn, while 40% said prior credit experience, 10% said emotional intelligence and 5% said a college degree.

Yes, but: Let’s take it back a few steps. The first and most important step from a hiring perspective is figuring out the right questions to ask. It is crucial to pinpoint what the role is and who will fit the best—and there is no better way to find out than by gauging the candidate’s experience and decision-making process. Here are some examples of questions to ask:

- How do you weigh relationship building with your internal (sales and operations team) and external customers?

- How do you determine credit limits and terms, if they aren’t standard, during the credit approval process?

- Provide an example of a time you had to make an immediate, yet major, company decision concerning credit. Also include the outcome of that decision.

- What credit reporting systems are you familiar with?

- Are you experienced in making business to business collection calls?

What they’re saying: Some credit professionals will ask softer questions after the technical ones. “After getting to know the potential candidate a bit more and learning about their experience, I like to ask ‘why should I hire you?’ or ‘what can you bring my organization that you believe is missing?,’” said Brian Diggs, director of credit at Power & Telephone Supply Company (Piperton, TN). “This gives me insight on how they view themselves in our company. I like to hear a healthy amount of confidence, without a know-it-all attitude.”

It is also essential to pinpoint the ideal traits of the role of a credit manager. Though this can differ from company to company, it ties into the bigger picture of finding the perfect fit. Some general examples of these traits can include:

- Financial literacy and analytical skills

- A strong appetite for learning

- Time management and comprehension skills

- Great communicators (people who like talking to people)

- Strong negotiation abilities

Different credit managers prioritize different skills in new hires. For example, the shift in attitude towards candidates who obtain a college degree versus those who do not has leveled the playing field. 10-15 years ago, a Bachelor’s degree was a confirmed ticket for success. Degrees now show employers you can complete long-term projects while you pursue your passion.

“When I go on to hire someone eventually, I’d want to see a college degree,” said Brittany Yvon, CBA, CICP, credit manager at OMG, Inc. (Agawam, MA). “A college degree mattered for me and my position, but it doesn’t have to be solely required to get hired. One of the benefits of college is the opportunity to join organizations and network and talk to people. There’s value in the community aspect and those skills can be translated into the work world.”

As the value of college degrees welters, credentials through certifications have exploded. Many credit managers will take a candidate who has a certification such as the Certified Business Fellow (CBF) or Credit Business Associate (CBA) over a candidate who has their Bachelor’s degree in an unrelated field. Credit management is not a specific degree; however, certifications are directly created for the field specifically.

A candidate’s willingness to learn is a skill that cannot be taught. Wanting to self-improve is an intrinsic characteristic that is valuable in the credit world especially because the role of a credit manager is never black-and-white. It takes skill knowing how to adapt and wanting to become multifaceted within your own role.

“I go in with a mindset that I will learn something new every day and I encourage that amongst my team,” said Nicole Butler, credit manager at Shakespeare Company LLC (Columbia, SC). “With learning, there is room to build relationships and pinpoint value-added tasks. I pay close attention to the potential candidate’s willingness in admitting their strengths and lack thereof, while being open to share those strengths with the team and willing to learn and build in areas where needed.”

Prior credit experience is a given for most credit managers because it is the financial heartbeat of a company. Being trained on the basics comes with entry-level, junior and senior experience—all needed for a management role. For example, some credit managers will specifically ask the portfolio size dollar amount the potential hire has dealt with previously. If the potential hire has only dealt with $100,000 accounts instead of multimillion dollar accounts, it may not be the right match for a company that only deals with Fortune 500 accounts.

“Experience is most important in this profession,” Butler said. “Experience encourages credit-minded decision-making skills. A lot of the day-to-day work involves supporting or making a credit decision that can affect all areas within the company. I also must consider if they will fit with the culture of the company department.”

Company culture is another key component in finding the right hire. Does the candidate work well in fast-paced environments? Do they have an extensive record of being able to multitask? Can they communicate clearly? Keeping the company’s values and culture in mind when interviewing a candidate can save time and investment. Joe Lange, CCE, ICCE, CCRA, senior credit manager at Brenntag North America, Inc. (Wauwatosa, WI), said emotional intelligence is the number one aspect that goes into company culture.

“You need to be able to develop the people you work with and give them your all through coaching them and being a mentor for all different personality types,” Lange said. “It takes a certain degree of emotional intelligence to be able to do that and realize that each of your people reacts and learns differently. As a manager, you need to be able to mold your training and mentoring to their personality type, not to your own personality type. I can teach someone how to be a good collector, or I can teach them how to be a good analyst, but you have to have those soft skills in front of you to be able to do that.”

The bottom line: The bottom line is that hiring in the credit profession requires a balance of technical skills, experience and personal attributes such as willingness to learn, adaptability and emotional intelligence, along with an alignment with company culture.

-

JUNE

24

3pm ET -

Uptiers, Dropdowns and Zombies – Oh My!

Speakers: Andrew Behlman, Partner and Colleen M. Restel, Esq., Counsel, Lowenstein Sandler LLP

Duration: 60 minutes

-

Quick Loans for B2B

Speakers: Nancy Hannah, Esq., Partner and Attorney, Hannah Sheridan Cochran, LLP

Duration: 60 minutes -

JUNE

25

3pm ET

-

JUNE

27

3pm ET -

Cyber Security 101: Fundamentals on Staying Safe in a Digital World

Speaker: Rebecca Bowen, Information Technology Operations Engineer

Duration: 60 minutes