Week in Review

October 8, 2018

Global Roundup

EU negotiators say Brexit deal “very close” but details missing. The European Union’s Brexit negotiators believe a divorce deal with Britain is “very close,” diplomatic sources said, in a sign that a compromise on the most contentious issue of the future Irish border might be in the making, though details were scarce. (Reuters)

Analysts see more risks than hope in Italy budget plan. Italy's expansionary multi-year budget plan published late on Oct. 4 may backfire on the populist government, according to several analysts who see a risk of rising borrowing costs, a bruising battle with Brussels and ratings downgrades. (Euronews)

USMCA to reduce North American corporates' trade risk. Ratification of the new U.S.-Mexico-Canada Agreement (USMCA) would significantly reduce the trade uncertainty for numerous North American corporate sectors that resulted from protracted renegotiations of the North American Free Trade Agreement (NAFTA). (Fitch)

Trump’s tariffs: How will U.S. construction fare? President Donald Trump’s protectionist trade policies were initially intended to help the United States, and there are arguments that certain industries will benefit. Yet there are some sectors that report that they’d be hurt by his protectionist policies. The truth lies somewhere down the middle according to certain analysts. (Global Trade Magazine)

China manufacturing weakens as tariff war with U.S. escalates. China’s export orders shrank in September as a tariff battle with Washington over technology escalated, adding to downward pressure on the world’s No. 2 economy, two surveys showed on Sept. 30. (Business Mirror)

May plans to rush Brexit deal through Parliament. Prime Minister Theresa May’s officials are drawing up plans to rush her Brexit deal through Parliament in an attempt to head off a rebellion from her own party, according to people familiar with the matter. (Bloomberg)

Italy isn’t like Greece. It’s better and worse. The first’s economy is in better shape, but it’s also much bigger and poses a far greater systemic risk. (Bloomberg)

Ireland processing over 100 Brexit-related applications from finance firms. Ireland’s central bank has seen a surge in financial services firms seeking to set up or extend their operations in Ireland as a result of Brexit and is processing over 100 applications, its governor Philip Lane said on Oct. 4. (HSN)

Japan’s PM reshuffles Cabinet; foreign, trade ministers stay. Japanese Prime Minister Shinzo Abe reshuffled his Cabinet on Oct. 2, retaining key diplomatic and economy posts as Japan tackles tough trade talks with the U.S. (News & Observer)

NAFTA replacement USMCA settles key trade uncertainties. A deal between the Canadian, Mexican and U.S. governments for a revised trilateral free trade agreement should reduce key uncertainties for U.S.-Canada and U.S.-Mexico trade that have been in place since the U.S. announced its intention to renegotiate NAFTA. (Fitch)

UN Report: Trade war threatens outlook for global shipping. The outbreak of trade wars and increased inward-looking policies threaten the prospects for seaborne trade. The warning comes against a background of an improved balance between demand and supply that has lifted shipping rates to boost earnings and profits. (Global Trade Magazine)

Here’s why the Indian rupee may fall below 75 per dollar soon. On a slippery slope since 2018 began, the Indian rupee closed at its weakest level, 73.34 per dollar, on Oct. 3—and opened even lower at 73.78 on Oct. 4. It has already shed 15% this year, making it one of Asia’s worst-performing currencies. (Quartz)

U.S. policy on Venezuela formally shifting toward regime change. A bipartisan group of U.S. senators is considering a more aggressive approach toward Venezuela with a bill calling for human rights prosecutions and a major U.S. role in the country's recovery. (Stratfor)

Maduro regime unfazed by condemnation. In a historic rebuke, five Latin American nations urged the International Criminal Court (ICC) to investigate the regime of Venezuelan President Nicolas Maduro for human rights abuses. Though such a public denunciation is noteworthy, the most legitimate external threat to the Maduro regime comes not from its neighbors, but from Beijing. (Global Risk Insights)

U.S.-China trade war sees WTO slash trade growth forecasts. The World Trade Organization (WTO) has downgraded its growth expectations for global trade, for this year and next, in response to the ongoing U.S.-China trade war. (Global Trade Review)

Blockchain and trade finance: What’s happening in China? Perhaps it’s due to the well-oiled publicity machines of the jurisdictions around it, but China’s blockchain developments in trade finance have flown slightly under the radar. (Global Trade Review)

UAE export credit agency embraces Islamic finance. A new agreement between the UAE’s export credit agency Etihad Credit Insurance (ECI) and the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC) will seek to promote non-oil UAE trade through Islamic risk mitigation tools. (Global Trade Review)

Know the risks of using a documentary collection when exporting. A documentary collection works well for many export transactions and provides a measure of security for both importers and exporters. It does have risks, however, to both parties, and it can represent a poor method of payment for some transactions. (Shipping Solutions)

Key global events to watch in October. At the start of every month, the Global Observatory posts a list of key upcoming meetings and events that have implications for global affairs. (IPI Global Observatory)

-

JUNE

25

3pm ET -

Quick Loans for B2B

Speakers: Nancy Hannah, Esq., Partner and Attorney, Hannah Sheridan Cochran, LLP

Duration: 60 minutes

-

Cyber Security 101: Fundamentals on Staying Safe in a Digital World

Speaker: Rebecca Bowen, Information Technology Operations Engineer

Duration: 60 minutes -

JUNE

27

3pm ET

Turkish Economy Stuttering

Chris Kuehl, Ph.D.

The series of economic crisis situations in Turkey have been escalating, and the issues are becoming more and more destabilizing. The inflation rate has soared to more than 25%. Many assert it can continue to worsen as the country tries to regain control of the value of the currency. It has lost almost 40% against the dollar this year already. This has made imports very expensive. Given that Turkey imports food, fuel and other basic goods, the impact has been swift and dangerous for those in the country who lack the ability to adjust their own incomes to match these price hikes.

The crisis started when the government of Reccip Tayyip Erdogan got into a major dispute with the United States over how to handle the status of Fethullah Gulen, a radical cleric living in the U.S., and a U.S. religious leader who had ties to him. President Donald Trump demanded the release of the American. Erdogan refused unless the U.S. was willing to turn over the cleric who Erdogan has asserted was behind the coup attempt of a few years ago. The U.S. then took steps to impose tariffs on steel produced by Turkey. The subsequent trade war escalated. It has not helped Turkey’s cause that Erdogan has been putting pressure on Israel and siding with Bashar al-Assad of Syria.

The Erdogan government is sounding more desperate by the day with alternating blasts of collusion and attempts to blame the public for the damage done. The finance minister has tried to assert the inflation is due to hoarders and those who are reacting in panic, but it is plain this has not been the issue. Turkey has been busy alienating all of those who would once have been counted as allies due to the increased paranoia manifested by Erdogan. Transportation costs are up 38% in September alone due to the higher prices paid for oil; food costs are up by 28%; and overall, producer prices are up by a whopping 46.2%. This large jump will soon start to impact consumer prices as well.

Where this goes from here will depend a great deal on the outcome of the hearing for Andrew Brunson. If the Turkish courts simply decide to expel him and leave the issue behind, the markets will assume economic issues will return to normal and the lire will regain some of its strength. If Erdogan puts more pressure on the U.S. over the Gulenists, the situation will worsen very quickly and hyperinflation becomes a real possibility. Erdogan has been trying to create some kind of anti-Trump alliance between Turkey, Russia, Europe and China, but nobody has been taking the bait despite all of them having issues with Trump.

Beyond the issue of Brunson and his connection to Gulen, there is the Turkish opposition to what the U.S. has been doing with the Kurds. The U.S. has essentially approved the formation of a Kurdish stronghold in northern Syria that has linked up to some degree with the Kurds in Iraq. That leaves the Turkish Kurds as the one group left out. Erdogan still considers this ethnic war his chief priority. His willingness to bend and cooperate with the U.S. has been severely limited by his defiance, but it seems Turkey lacks any kind of leverage that would budge the U.S.

Join Bierens’ attorney, Omer Faruk Celik, as he reviews the legal, credit and collection environment in Turkey in an upcoming FCIB webinar, Doing Business in Turkey. Omer has been a registered member of the Istanbul Bar Association since 2011 and is the lead attorney for all commercial, litigation and bankruptcy matters throughout Turkey on behalf of all Bierens clients.

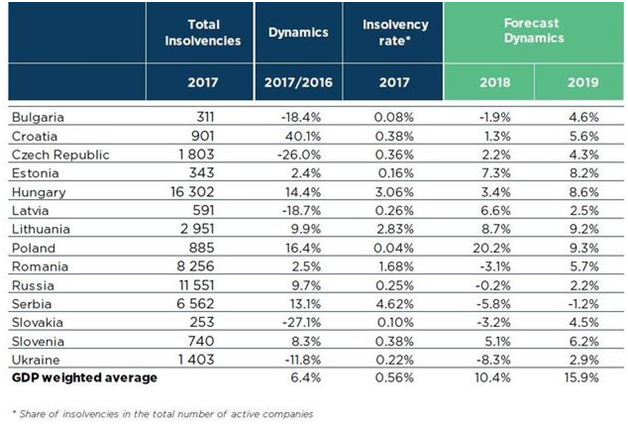

Central & Eastern European Insolvencies: The Good Times Are Over

Coface

The Central and Eastern European region (CEE) has been enjoying improved economic activity in recent years. This was particularly noticeable in 2017, when the region’s average GDP growth soared to 4.5%—the highest rate since 2008.

Household consumption and inputs from rebounding fixed asset investments made significant contributions to growth. Nevertheless, the favorable business environment in 2017 was not sufficient to drive an improvement in companies’ liquidity situations.

The overall number of insolvencies increased by 6.4% in 2017, which means a reversal of the trend shown in recent years, where there was a drop of 6% in 2016, following a fall of 14% in 2015. Another change was the fact that in 2017 more countries were affected by an increase in insolvencies. During the year, a higher volume of insolvencies was reported in nine countries: Croatia, Estonia, Hungary, Lithuania, Poland, Romania, Russia, Serbia and Slovenia. A decrease was reported in five countries: Bulgaria, Czech Republic, Latvia, Slovakia and Ukraine.

Source: Coface

The regional breakdown reveals a wide variety of dynamics, ranging from a 27.1% decrease in insolvencies in Slovakia and a drop of 26% in Czech Republic, to slight increases of 2.4% in Estonia and 2.5% in Romania and even a surge of 40.1% in Croatia. The countries shared some common reasons for the deteriorating business liquidity that has led, in some cases, to insolvencies.

“High capacity utilization and solid demand encouraged companies to expand their capacities,” explained Grzegorz Sielewicz, regional economist Coface Central and Eastern Europe. “In addition to this, positive periods in the economy motivated new businesses to set up, despite the high level of competition prevailing in a number of sectors. Companies frequently experienced increases in turnover, but lesser increases in profits. Profits were constrained by rising costs, including wage growth and the higher costs of inputs—as confirmed in accelerating producer price indexes.”

Furthermore, difficulty in filling job vacancies became a major obstacle for businesses in the CEE region in their activity and potential expansion. Companies more frequently reported this barrier as being a concern, than the uncertainty surrounding demand for their products and services, according to Eurostat’s business surveys. Coface therefore concludes that economic acceleration is not the only factor affecting the liquidity of the region’s business sector.

For 2018 and 2019, Coface forecasts continued increases in the number of regional insolvencies. This confirms the end of an economic cycle in Central and Eastern Europe. 2018 will see the average number of insolvencies rise by 10.4%, with more countries recording an increase in proceedings. Poland is expected to record a hike of 20.2% in business insolvencies and restructuration proceedings. Serbia and Slovakia, on the other hand, will experience a contraction in insolvencies. Weaker economic growth will be a contributing factor to CEE average insolvencies expanding by 15.5% in 2019.

Election Calendar

Luxembourg, Chamber of Deputies, Oct. 14

Afghanistan, House of People, Oct. 20

Georgia, President, Oct. 28

Trade Deal Averts Potential Trade Nightmare

Atradius

Canada has joined Mexico and the United States in a new trade agreement, averting a potentially massive hit to trade, profits and employment in North America.

The new North American Free Trade Agreement (NAFTA) will be called USMCA (United States Mexico Canada Agreement). Here are some of the major headlines under the new agreement.

The economic effects of USMCA are likely to be limited, as it is widely seen as a rebranding of NAFTA than an entirely new deal. Markets will be relieved, though, that trade between the major three countries will keep flowing. Rules of origin have become more demanding for auto manufacturers because the percentage of regional auto production will be gradually increased from 62.5% to 75%.

It is expected that local Canadian, Mexican and U.S. suppliers will benefit from increasing the regional content of vehicle production, as OEMs [original equipment manufacturers] would be inclined to make new contracts. Additionally, 40% to 45% of final automotive assembly has to be done by workers earning an average of $16 an hour or more. While this is aimed at Mexico (Mexican workers in the automotive industry earn $3.5 an hour on average), it seems most probable that businesses in Mexico will keep the competitive advantage of low labor costs and accept instead a foreseen additional 2.5% tariff. Additionally, quotas will increase leaving more room for growth.

Of the Canadian dairy market, 3.6% will be opened to U.S. products. Stricter definitions on what is included in this quota will need to be added, however. Expectation is that dairy prices in Canada will fall somewhat as a result of the increased competition from U.S. and other markets via the 3.25% access granted in CPTPP [Comprehensive and Progressive Agreement for Trans-Pacific Partnership] agreement. This does keep in place supply chain management, however there are wide differences in opinions on the extent to which it remains. The dispute settlement provision will be kept in place, which is a victory for Prime Minister Trudeau. A notable exclusion from the agreement is the inclusion of language on steel and aluminum exports to the United States.

Bottom line, the agreement will keep trade in North America flowing and should strengthen business between the three countries. Agriculture may experience a tightening of margins and is an industry to pay close attention to in 2019 once the agreement is ratified. Steel and aluminum businesses will remain on our watch list until an agreement on tariffs is reached. This also extends to industries reliant on steel and aluminum.

Week in Review Editorial Team:

Diana Mota, Associate Editor and David Anderson, Member Relations